Russian Arms Transfers and Asian Military Modernisation

29 Dec 2015

By Richard A. Bitzinger for RSIS

This policy Report was external pageoriginally published by the external pageS. Rajaratnam School of International Studies (RSIS) on 15 December 2015.

Introduction

The Russian defence industry is a critical segment of the country’s economy, employing at least 2.5 million workers, and accounting for 20 per cent of all manufacturing jobs. The arms industry suffered considerably after the collapse of the Soviet Union in the early 1990s and subsequent years of neglect due to a precipitous drop in military spending. According to data put out by the Stockholm International Peace Research Institute (SIPRI), defence spending (in constant 2011 U.S. dollars) fell from US$371 billion in 1988 to a low of US$21 billion in 1998. The resulting plunge in Russian defence procurement spending meant that the Russian arms industry had to find overseas customers or else face extinction. By the early 2000s, therefore, the Russian arms industry reportedly relied on arms exports for up to 80 per cent of its income, and securing overseas buyers was absolutely critical to the survival of the Russian defence industry.[1]

By the late 2000s, however, Russian defence spending began to rise again, spurring a revitalisation of the arms industry. Between 2004 and 2014, military expenditures grew from US$41 billion to US$91.7 billion (in constant 2011 U.S. dollars), according to SIPRI data; approximately 40 per cent of spending goes to procurement, leading to a resurgence of domestic orders for armaments from Russia’s arms industries. [2] Consequently, currently 75-80 per cent of defence industry output is for the Russian military, and about 20-25 per cent is exported.

While arms exports are not nearly as essential as before, they are nevertheless still important to the continued well-being of the Russian defence industry. After the collapse of the Soviet Union, Russia’s share of all global arms transfers fell to around 12 per cent (according to SIPRI); starting around 2000, however, Russian defence exports began to recover, and by 2014 it held a 27 per cent share in the global arms market, second only to the United States.[3] According to Russian sources, in 2014 Russian defence firms exported more than $15 billion worth of arms to more than 60 countries, and signed almost $14 billion worth of new contracts.[4] It is worth noting that the depreciation of the Russian ruble has actually aided overseas arms sales, as Russian arms exports are paid for in foreign currencies (which are then converted back into rubles, earning higher revenues).[5]

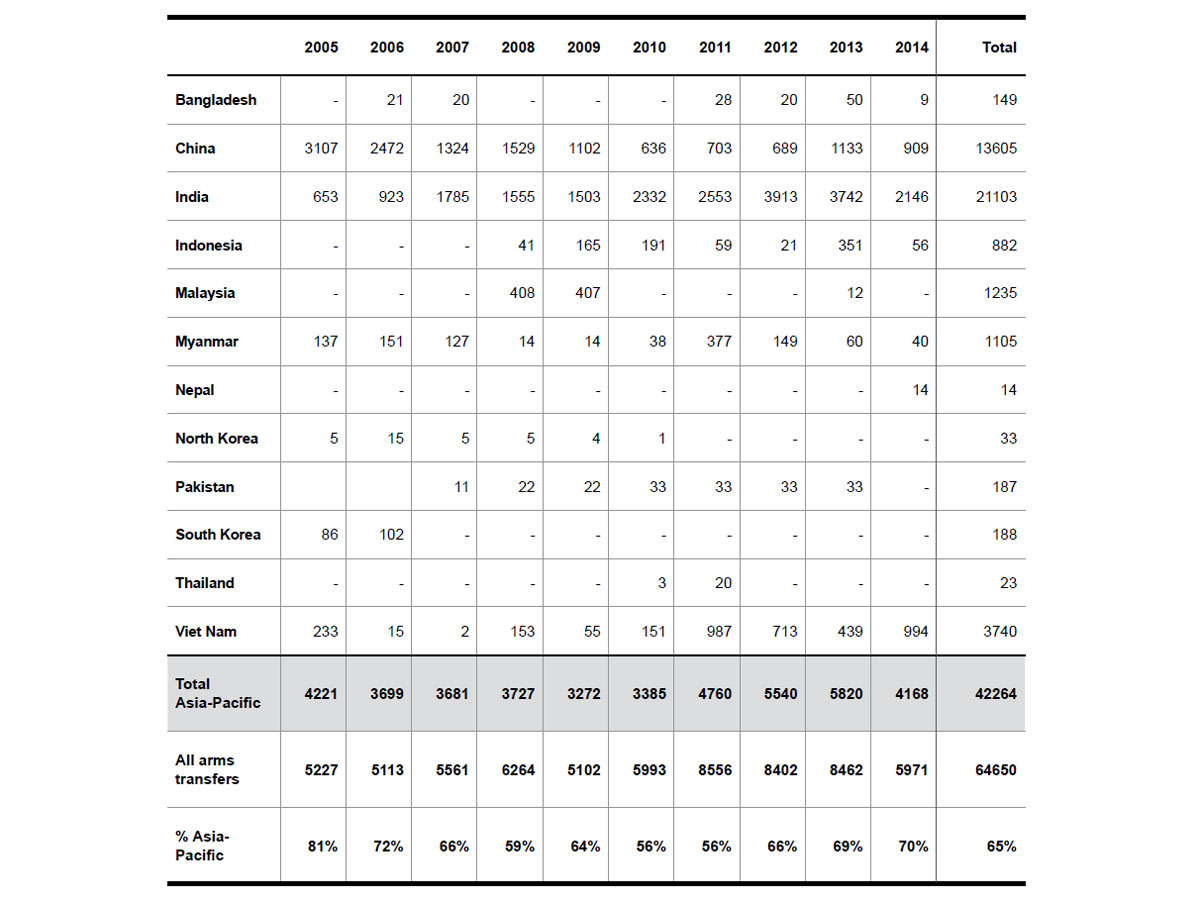

In this regard, the Asia Pacific market has been particularly crucial for Russian overseas arms sales. The Asia Pacific is still Russia’s single most important market, despite some diversification of buyers. Between 2005 and 2014, nearly two-thirds of all Russian weapons exports, worth approximately US$42.3 billion, were to this region, according to SIPRI (Figure 1). In particular, this region contains Russia’s two largest arms buyers, India and China, who together account for over half of all Russians transfers period (32 per cent and 21 per cent, respectively). Vietnam is also a traditional customer, buying US$3.7 billion worth of Russian armaments over the past decade. More critically, however, over the past decade Moscow has been able to expand its customer base within the Asia Pacific, especially within Southeast Asia. In recent years, it has found new buyers in Indonesia, Malaysia, Myanmar, and Thailand.

In addition to off-the-shelf arms sales, Russia has begun to promote technology transfers, joint research and development (R&D), and coproduction of defence items with partnering arms-manufacturing countries, particularly India and China. Russia, for example, is offering to coproduce jet engines with its Indian counterparts, building on earlier fighter and missile joint production agreements.[6]

Table 1:Value of Russian Arms Transfer to the Asia-Pacific, 2004-2014 (in millions of constant 1990 U.S. Dollars)(click to enlarge) Source: SIPRI Arms Transfers Database

China

The USSR was China’s most important arms supplier from the birth of the People’s Republic up to the Sino-Soviet split in 1960. Russian arms sales to China were not renewed until the early 1990s, when Beijing began to import large quantities of advanced weapons from Russia. Since the early 1990s, China has acquired nearly US$60 billion (in 2015 dollars) worth of arms from Russia, about three-quarters of all its arms imports over the past 25 years. In particular, up until quite recently, Russian systems constituted the most advanced weaponry found in the People’s Liberation Army (PLA).

In 1991, China ordered 24 Russian-built Su-27 fighter jets; this was subsequently complemented by the purchase of additional Su-27s, and later the more advanced Su-30MKK and Su- 30MK2. Beginning in the early 2000s, China later produced, under license, a version of the Su-27 (designated the J-11) at the Shenyang Aircraft Company in Manchuria These combat aircraft are also equipped with Russian-supplied weaponry, including the RE-77E (AA-12) active-radar guided air-to-air missile (AAM), the Kh- 59MK antiship cruise missile (ASCM), and the Kh-31P anti-radiation missile. In the late 1990s and early 2000s, the PLA Navy (PLAN) also acquired four Sovremennyy-class destroyers from Russia. Of particular note, these ships are outfitted with the 3M-80E Moskit (SS-N-22 Sunburn) ramjet-powered, supersonic ASCM, which has a range of 120 kilometers; later-model Sunburns have a 200-kilometer range. During the same period, China bought 12 Kilo-class diesel-electric submarines from Russia; these submarines are armed with the 3M-54E Klub (SS-N-27) ASCM and the 53-65KE wake-homing torpedo. Other critical Russian arms transfers to China include the S-300 and S-400 surface-to-air missile (SAM), Hip helicopters, and Il-76 cargo aircraft.

Of special note, Russia indirectly supplied China with its first aircraft carrier, the former Soviet Varyag. A casualty of the post-Cold War, the Varyag was laid down in the early 1980s, but construction was halted in 1992 when the vessel was only 70 per cent complete. Ukraine, which inherited the Varyag after the breakup of the Soviet Union, sold it to China in 2001, ostensibly to be turned into a Macau casino. However, the Chinese moved the vessel to a drydock at the Dalian shipyard in northeast China, where it underwent substantial repairs and reconstruction, along with the installation of new engines, radars, and electrical systems. The rebuilt ex-Varyag carrier underwent its first sea trials under PLAN colors in August 2011, and it was subsequently commissioned the Liaoning and accepted into service with the PLAN in 2012. The Liaoning is equipped with the J-15 fixed-wing fighter jet (reportedly reversed-engineered from a Su-33 acquired surreptitiously from Ukraine), along with anti-submarine warfare and airborne early warning helicopters.

Despite a recent reduction in arms purchases from Russia, China is still buying about US$2 billion worth of armaments from Russia. In particular, Russia has become a critical supplier of key subsystems and military technologies to China. In particular, China still has to import advanced jet engines from Russia for its indigenous J-10 fighter, as well as its J-11B combat aircraft (a reverse-engineered version of the Su-27). Chinese-built frigates and destroyers incorporate Russian radar, naval guns, missile components (such as seekers), and helicopters. Technical cooperation with China is also replacing off-the-shelf sales. According to the U.S.-China Economic and Security Review Commission, China and Russia are cooperating in the joint-design and production of advanced diesel-electric attack submarines containing Russian sonar, propulsion, and quieting technology. [7]

Moscow is not overly concerned about arms sales to China negatively affecting Russian security. There is a general feeling that China is not a significant threat to Russia. China’s growing preferences to build up its navy means that Beijing is looking south, not north – i.e. away from Russia. At the same time, Russia’s nuclear forces are deemed sufficient to deter any possible Chinese threats to Russia’s land border and geostrategic interests. Consequently, the Russian-Chinese relationship is viewed to be a mutually beneficial one, and Moscow is hopeful that it can continue to supply critical systems and subsystems (e.g. missiles, jet engines, ship turbines, etc.) that will go into indigenous Chinese weapons platforms. [8]

India

Perhaps no country has been more dependent on Russian arms imports than India. According to SIPRI, India received 70 per cent of its arms imports from Russia in recent years (2010-2014). Despite possessing a huge indigenous defence industry, and despite literally decades of effort put into developing and manufacturing its own advanced armaments, India continues to depend heavily upon Russia for the most sophisticated weaponry in its arsenal. Major Russian weapons systems found in India’s military include the Su- 30MKI fighter-bomber, the T-90 main battle tank, the BMP-2 infantry fighting vehicle, the 9M113 Konkurs anti-tank missile, the Ae-50 airborne early warning aircraft, Kh-35 and 3M-54 Klub ASCMs, and RE-73 and RE-77 AAMs.

New Delhi is also working to create a national missile defence system incorporating the Russian S-300 surface-to-air missile and a variety of indigenously developed exoatmospheric and point-defence missile systems, together with the Israel Green Pine active phased array radar.

In addition, the Indian navy is in the process of acquiring a long-desired aircraft carrier from the Russians, in this case, the Soviet-built Admiral Gorshkov, a 45,000-ton Kiev-class carrier, decommissioned by the Russian Navy in 1996. After years of negotiations, Moscow and New Delhi agreed to a deal whereby Russia would provide the carrier gratis, while India would pay the Russians approximately $1 billion to refit and upgrade the vessel to be capable of flying navy MiG-29 fighters off its deck in a STOBAR (short take-off but assisted recovery) configuration. This entailed stripping off the weaponry from the ship’s foredeck and adding a 14 degree ski-jump on the bow and three arrestor wires on the angled landing deck. In addition, India will pay another $700 million towards the aircraft and weapons systems, which include 12 single-seat MiG-29K Fulcrum-D fighter jets, four dual-seat MiG-29KUB trainer aircraft, and six Kamov Ka- 27 and Ka-31 helicopters, along with training, simulators, spare parts, and maintenance facilities. The carrier, which is renamed the INS Vikramaditya, was supposed to have been delivered to the Indian Navy in mid-2008, but refitting the vessel has turned out to be much more challenging than originally envisioned, resulting in considerable cost overruns and delays. Ultimately, the Vikramaditya cost nearly three times its original price and entered service in 2013, several years behind schedule.

In addition to off-the-shelf arms sales, Moscow has permitted India to license-produce many Russian-designed weapons systems. India currently manufactures the Su-30 combat aircraft from complete knock-down (CKD) kits, the T-90 tank, the BM-9A52 Smerch multiple-rocket launcher, and the tank-launched, laser-guided 9M119 Svir/AT-11 anti-tank weapon. More importantly, Russia and India have also begun to explore joint R&D and production of new weapons systems. The supersonic BrahMos cruise missile, for example, is the product of a joint venture between India’s Defence Research and Development Office (DRDO) and Russia’s NPO Mashinostroyenia. In addition, in 2006, Russia’s Irkut Corporation entered into a U$700 million joint venture with Hindustan Aeronautics Ltd. (HAL) to design and build a 60-ton multirole transport aircraft (MTA).

Most important of all, perhaps, Moscow and New Delhi have agreed to co-develop a fifth-generation fighter (FGFA) based on the Russian PAK FA programme, which in turn is based on the Sukhoi T-50 prototype. Under the terms of this joint venture, HAL will work with Sukhoi to develop a two-seater version of the T-50, in exchange for a 25 per cent workshare in the aircraft’s design and development, including the mission computer, navigation systems, cockpit displays, and countermeasure systems. The project will also entail considerable Russian technology transfers to India. Altogether, New Delhi could invest up to US$35 billion into the FGFA, including R&D and the procurement of 250 aircraft. Russia and India would also set up a joint marketing company to export this fighter.[9] India participation in the FGFA is particular important to Russia’s aircraft industry, as Indian production of the Su-30MKI is set to conclude by the end of next year.

Southeast Asia

Russia sees Southeast Asia as a prime market for its armaments. This is aided in part by the fact that many countries in this region want to diversity their suppliers away from any possible over-dependency on the United States (this has also helped Western European and Israeli arms exports to this area). [10] Russian arms do not come with as many political strings, while at the same time Russia prefers be a low-key player in the region. Potential Russian arms sales to Southeast Asia include: air-defence missiles, ASW ships, antiship cruise missiles, helicopters, offshore patrol vessels (OPVs – i.e. corvette-sized vessels for long-endurance patrolling), and perhaps submarines.

Indonesia

Indonesia is seen as particularly having a lot of potential for Russian arms sales. Indonesia’s most important arms acquisitions from Russia have been of fighter aircraft. In the late 1990s, Jakarta had intended to procure 24 Su-30MK fighter-bombers, but this order was cancelled in the wake of the 1997 Asian financial crisis. Eventually, Indonesia did acquire five Su-27s and 11 Su-30s. These are equipped with short- and medium-range AAMs, as well as air-to-surface and anti-ship missiles. The Indonesian Air Force (TNI-AU) has a requirement for several more fighters, which could be filled by the purchase of additional Russian combat aircraft (although the TNI-AU recently bought 30 ex-US Air Force F-16C/Ds, at a cost of US$600 million, and it will use these aircraft to equip two new fighter squadrons).

Other Russian arms imports include BMP- 3 infantry fighting vehicles, Hip helicopter gunships, and the Yakhont ASCM, to be outfitted on Indonesian frigates. At one time, Indonesia had planned to acquire several Kilo-class and Lada-class submarines from Russia, to replace its two aging German-built Type-209 boats; this deal fell through after the two sides failed to agree on financing arrangements, and Jakarta subsequently purchased three submarines from South Korea.

Malaysia

In 2003, the Royal Malaysian Air Force (RMAF) ordered 18 Su-30MKM Flankers from Russia – at a cost of US$900 million – to complement its existing force of 18 MiG-29 Fulcrums (which are armed with the active radar-guided AA-12 air-to-air missiles) acquired in the early 1990s (along with eight F/A-18Ds from the USA). The RMAF has an outstanding requirement for another 18 fighter aircraft, with could entail the purchase of additional Su-30s (although the Swedish Gripen and the F/A-18 are also potential competitors for this contract).

Vietnam

Vietnam is Russia’s third-most important arms customers in the Asia Pacific, after China and India. The Vietnamese navy is currently taking delivery of six Kilo-class diesel-electric submarines from Russia, at a cost of US$2 billion.[11] The navy has acquired four Gepard-class frigates (armed with Kh-35 ASCM) and six Svetlyak-class patrol craft, and it is producing several Russian-designed Tarantul-class corvettes under license. The Vietnam People’s Air Force (VPAF) has been attempting to modernise its arsenal since the early 1990s, buying Sukhoi Su-27 fighter aircraft in the mid- 1990s, and then, beginning in the 2000s, the much more capable Su-30MKK, but this process has been slow and modest. Up until 2013, it had procured only 12 Su-27s and just 24 Su- 30MKKs, although it was recently announced that the VPAF intended to acquire an additional 12 Su-30s.

Vietnam is also relying heavily upon Russian arms to build up its air and coastal defence capabilities, ostensibly to guard against China. It has acquired the S-300 SAM, and it is currently procuring the more advanced S-400 version. It has also bought several hundred Igla-1 man-portable SAMs. In 2011, Vietnam acquired the K-300P Bastion-P coastal defence system, based on a vehicle-mounted Yakhont ASCM.

Conclusion

The Russian arms industry is presently experiencing something of a renaissance. The defence sector has continued to grow, despite the growing impact of falling oil prices and Western sanctions (imposed after Moscow’s annexation of Crimea) on the overall Russian economy.[12] Domestic military procurement spending is up considerably, reaching US$26.3 billion in 2014.[13] At the same time, overseas arms sales have remained strong, hitting US$13.2 billion that same year. [14] Russia’s aircraft and air-defence (missile) sectors have been particularly powerful performers. For example, Russia’s United Aircraft Corporation (UAC, which incorporates the Sukhoi, Mikoyan, Ilyushin, Yakolev, Beriev, Irkut, and Tupolev aircraft firms), has achieved remarkable success in recent years, both in terms of number of aircraft produced and in terms of sales. UAC produces about 200 aircraft a year, both military and civilian, although 80 per cent of UAC’s revenues currently come from military sales. Most of its output used to be exported, but currently purchases by the Russian military account for 80 per cent of UAC’s income (mostly Su-27/-30/-35 fighters, as well as upgrades of MiG-29s). [15]

Even with the recovery of the domestic arms market, the Russian defence industry still craves export sales. Besides being a source of foreign hard currency and additional profits, overseas arms sales serve as a hedge against future possible downturns in Russian military procurement, especially should the growing economic crisis that is beginning to grip Russia lead to defence spending cuts. Despite prior assurances by Putin that the defence budget would be shielded from planned 10 per cent government-wide spending reductions, the decline in world oil prices and Western sanctions could force a change in policy.[16]

Western sanctions on Russia could also soon affect the defence industry. These restrictions have halted not only Western military exports (which help fill critical gaps in Russia’s defence capabilities) but also commercial high-tech transactions that could have dual-use military applications. As one analyst puts it: “Moscow saw these imports as a means, through the transfer of Western technologies and manufacturing practices, of making Russia’s defence industry more competitive in the global defence marketplace.”[17]

The Russian defence industry faces critical structural challenges as well, including inflation, high levels of debt, and the loss of qualified personnel. For example, inflation, currently running at around 15 per cent – and it is alleged that in certain weapon categories the figure was more like 30 per cent – has eaten up much of Russia’s military procurement budget.[18] Many defence firms are still struggling to achieve profitability. More important perhaps, the manpower base within the Russian defence industrial base is aging rapidly; the average age of its scientists and engineers is now around 50 years, meaning that, in a few years, the Russian defence industry could face a severe shortage of technical personnel.[19]

Consequently, the Russian arms industry could find that, once again, exports are more necessary than ever. In its efforts to secure increased overseas arms sales, certain factors are in its favour. Russian arms are reliable and relatively easy to operate. In addition, the Russian defence industry is increasingly emphasising after-sales servicing, so MRO (maintenance, repairs, and overhaul) and upgrades are increasingly on hand. [20] Most important of all, perhaps, Moscow offers many types of very capable weapons systems (such as the Su-30 multirole fighter and the S-300/- 400 air-defence missile) with few restrictions and at very competitive prices. At the same time, Russia is continuing to develop the kinds of products that could find a welcomed niche in the global arms market, even though many of these systems are being developed for local requirements.[21] Moscow, for example, could easily market its T-50 fifth-generation fighter as a cheaper alternative to the U.S. F-35 Joint Strike Fighter.

The Asia Pacific, including Southeast Asia, will continue to be a prime market for Russian arms sales. At the same time, former Soviet states – especially those now under the new Moscow-led Collective Security Treaty Organization (CSTO) – along with African countries, are likely to become growing customers for Russian arms. In general, therefore, one should expect that Russia would be an increasingly powerful player in the global arms market.

In turn, Asia Pacific militaries will likely find Russian armaments to be an ever more appealing alternative to Western weapons systems. Russian weaponry is increasingly competitive when it comes to capability, quality, and costs. Particularly in the relatively open arms market that is Southeast Asia, therefore, Russian armaments should find an increasingly receptive welcome.

Notes[1] Author’s interviews in Moscow, September 2015.

[2] Author’s interviews in Moscow, September 2015.

[3] Pieter D. Wezeman and Siemon T. Wezeman, Trends In International Arms Transfers 2014, SIPRI Fact Sheet (Stockholm: Stockholm International Peace Research Institute, March 2015), p. 2.

[4] Gabriela Baczynska, “Putin: Russia’s 2014 Arms Sales Top $15 Billion,” Reuters, January 27, 2015.

[5] Author’s interviews in Moscow, September 2015.

[6] Richard Weitz, “Russia’s Defence Industry: Breakthrough or Breakdown?” International Relations and Security Network (ISN), March 6, 2015; author’s interviews in Moscow, September 2015.

[7] 2014 Report to Congress of the US-China Economic and Security Review Commission (Washington: US Government Printing Office, November 2014), p. 302.

[8] Author’s interviews in Moscow, September 2015.ing Office, November 2014), p. 302.

[9] Ajal Shuka, “India, Russia close to pact on next generation fighter,” Business Standard, January 5, 2010 (external pagehttp://www.business-standard.com/india/news/india-russia-close-to-pactnext-generation-fighter/381718. )

[10] Author’s interviews in Moscow, September 2015.

[11] Nga Pham, “Vietnam to Buy Russian Submarines”, BBC News, 16 December 2009.

[12] Christopher Harress, “Russia’s Defence Sector Shows Major Growth,” International Business Times, July 15, 2015;

[13] Andrey Frolov, “Russian Defence Procurement in 2014,” Moscow Defence Brief, #3 (47), 2015, pp. 20-21.

[14] Anna Dolgov, “Russian Arms Sales up Despite Sanctions,” Moscow Times, April 13, 2015.

[15] Author’s interviews in Moscow, September 2015.

[16] Weitz, “Russia’s Defence Industry: Breakthrough or Breakdown?”

[17] Weitz, “Russia’s Defence Industry: Breakthrough or Breakdown?”

[18] Margarete Klein, Russia’s Military Capabilities: “Great Power” Ambitions and Reality (Berlin: Stiftung Wissenschaft und Politik, October 2009), pp. 26-28; “Analysis: Russian Budget Suffers Corrosive Effects of Inflation,” Jane’s Defence Industry, August 8, 2008.

[19] Author’s interviews in Moscow, September 2015.

[20] Author’s interviews in Moscow, September 2015.

[21] Author’s interviews in Moscow, September 2015.